Latest Insurance Quote

-

ttc

- Team Black

- Posts: 2893

- Joined: Fri Nov 19, 2004 2:59 pm

- Bike: Z1000

- State: Queensland

- Location: Brisbane

Re: Latest Insurance Quote

you could always be me.. my insurance will cost me $450 full comp on the zed.. it's not what you know it's who

Re: Latest Insurance Quote

I found Shannons heaps cheaper than WQBE, plus shannons does riding gear worth $3,000 and agreed value, and no extra to pay by the month. I pay around $700 - $800, and Im a hooligan..go figure

When I asked Wqbe to match the quote they couldn't ???? which is against their policy I think

When I asked Wqbe to match the quote they couldn't ???? which is against their policy I think

-

Frank

- KSRC Contributor

- Posts: 1432

- Joined: Tue Jun 07, 2005 10:23 pm

- Bike: ZX9R

- State: New South Wales

- Location: Shaggers Ridge, Sydney

Re: Latest Insurance Quote

When I Asked them to match it they came back with a better price, even with PBTMhoffy wrote:I found Shannons heaps cheaper than WQBE, plus shannons does riding gear worth $3,000 and agreed value, and no extra to pay by the month. I pay around $700 - $800, and Im a hooligan..go figure

When I asked Wqbe to match the quote they couldn't ???? which is against their policy I think

GO THE BLUES

Life time member of PETA:-

PEOPLE for the EATING of TASTY ANIMALS

Member of SRT

1998 Kawasaki ZX9R Track Bike

2014 Nissan Navara

Life time member of PETA:-

PEOPLE for the EATING of TASTY ANIMALS

Member of SRT

1998 Kawasaki ZX9R Track Bike

2014 Nissan Navara

Re: Latest Insurance Quote

OK, I might try them again...see what they say.frl0173 wrote:When I Asked them to match it they came back with a better price, even with PBTMhoffy wrote:I found Shannons heaps cheaper than WQBE, plus shannons does riding gear worth $3,000 and agreed value, and no extra to pay by the month. I pay around $700 - $800, and Im a hooligan..go figure

When I asked Wqbe to match the quote they couldn't ???? which is against their policy I think

-

ZXRobyn

- KSRC Contributor

- Posts: 1131

- Joined: Mon Jan 08, 2007 11:21 am

- Bike: ZX9R

- State: New South Wales

- Location: Oatley, Sydney NSW

- Contact:

Re: Latest Insurance Quote

Far out - I knew I'd cop it for that.....ZXRobyn wrote:just posting this as a note to the older riders with more sedate bikes(that sounds wrong, but you know wot i mean

FTR I'm one of the older riders - ok maybe not a low risk bike...

You might want to read the fine/small print with IMR - I remember someone referring to it on a different email forum??? Anyway I'd check it out to make sure there's no 'hidden surprises'.

Ok, I'm crawling back into my box now

Four wheels move the body. Two wheels move the soul.

HCST #1

-

robracer

- VIP MEMBER

- Posts: 15251

- Joined: Thu Feb 24, 2005 8:23 pm

- Bike: ZX6R

- State: New South Wales

- Location: Port Macquarie

Re: Latest Insurance Quote

ZXRobyn wrote:Far out - I knew I'd cop it for that.....ZXRobyn wrote:just posting this as a note to the older riders with more sedate bikes

Sedate: What I meant or should have said was 'with bikes that are considered 'lower risk' from the underwriters perspective that is'!!

FTR I'm one of the older riders - ok maybe not a low risk bike...

You might want to read the fine/small print with IMR - I remember someone referring to it on a different email forum??? Anyway I'd check it out to make sure there's no 'hidden surprises'.

Ok, I'm crawling back into my box now

Re: Latest Insurance Quote

Basing your insurer solely on cost of a Policy will become a recipe for disaster

come claim time.

come claim time.

-

Shifty

- KSRC Regular

- Posts: 834

- Joined: Tue Apr 26, 2005 9:04 pm

- Bike: ZX12R

- State: Queensland

- Location: Brisbane

Re: Latest Insurance Quote

Finally, some wisdom on the internets!MG wrote:Basing your insurer solely on cost of a Policy will become a recipe for disaster

come claim time.

Definitely worth looking into what is and is not covered. A saving of $250 can easily be un-done when you have a claim and find out that your $800 helmet isn't covered, or you only have cover for a few hundred bucks.... and there are a bazillion other things that may rock/suck about a particular policy so there is no substitute for sitting down with a coffee (beer?) and reading the policy booklets cover-to-cover.

-

Benno

- KSRC Contributor

- Posts: 1241

- Joined: Fri Jul 15, 2005 4:33 pm

- Bike: Scooter

- State: Victoria

- Location: Melbourne!!

Re: Latest Insurance Quote

I went with Shannons and had to make a claim. Very easy and straight forward. Only advice I can give you is: DON'T LIE ABOUT ANY OF YOUR DRIVING HISTORY. They will find out. And they will negate your claim.

Shannons were the cheapest by a long way.

Shannons were the cheapest by a long way.

Vespa!

-

Shifty

- KSRC Regular

- Posts: 834

- Joined: Tue Apr 26, 2005 9:04 pm

- Bike: ZX12R

- State: Queensland

- Location: Brisbane

Re: Latest Insurance Quote

Spot on. Insurers can't actually access your driving history, but they have a right not to pay out on a claim until you provide them with an up-to-date copy of it to confirm that the information you provided was true/correct/complete.

-

mike-s

- Apprentice Post Whore :-)

")

- Posts: 6142

- Joined: Sat Aug 07, 2004 5:43 am

- Bike: Suzuki

- State: New South Wales

- Location: Arncliffe, Sydney

- Contact:

Re: Latest Insurance Quote

Agreed, i got the gsx250 registered today and when i got 3pp insurance i was asked the whole raft of questions about my driving history, suspended/disqualified.

I figured to hell with it and admitted that i got suspended for 3 months for speeding.

Surprisingly i don't believe that it made an impact on how much it cost me for the insurance. I did an estimate earlier and it came across as $19/month when i did an online estimate. In reality it cost me 20.54 a month. Which is pretty close (just on 10% more). I would have expected maybe 25/month, but i guess its not made as much of an impact as i thought.

I figured to hell with it and admitted that i got suspended for 3 months for speeding.

Surprisingly i don't believe that it made an impact on how much it cost me for the insurance. I did an estimate earlier and it came across as $19/month when i did an online estimate. In reality it cost me 20.54 a month. Which is pretty close (just on 10% more). I would have expected maybe 25/month, but i guess its not made as much of an impact as i thought.

If it hurts, you aren't doing it right.

Re: Latest Insurance Quote

Exactly right bud.Shifty wrote:Finally, some wisdom on the internets!

Definitely worth looking into what is and is not covered. A saving of $250 can easily be un-done when you have a claim and find out that your $800 helmet isn't covered, or you only have cover for a few hundred bucks.... and there are a bazillion other things that may rock/suck about a particular policy so there is no substitute for sitting down with a coffee (beer?) and reading the policy booklets cover-to-cover.

I'll use a well known insurer to illustrate, but the same will apply to

any insurer if you are only focused on the cost or a Policy rather

than actually researching/studying the product on offer.

wQBE wanted the excess upfront even though I provided proof that it was a not-at-fault claim. They explained that every claim they process they ask for excess up front. My excess was $750, $500 standard and $250 inexperienced rider excess. I explained that I was hit from behind giving way to a pedestrian at a pedestrian crossing and that inexperience wasn't a factor, they explained that regardless of whether inexperience was a factor or not they always charge this where applicable.

A wQBE said that although I was not at fault even if I did pay my excess and was found not at fault I may not see my excess back, it depends on if the other party feels like paying it. Seems like a waste to pay $750 make a claim on an exhaust, only to have my premiums increase.

MG wrote:Couple of points for you matey:

An excess is an amount (contribution) you must pay when

YOU make a claim. Getting it back/having it waived etc is a

seperate, but related topic.

Some insurers will always ask for it up front (regardless of

whether you are at fault or not). It depends on their guide-

lines.

I see nothing untoward with QBE asking you to pay all excesses

up front (& you'll see why).

In regards to your Inexperienced excess, they'll charge that

as long as you have not held a bike license for 3yrs. Period.

The type of incident you had &/or who was at fault is irrelevant.

Again this is how they operate their product & furthermore, its

something you agreed to (unfortunately)

Having said that, your post illustrates why its important to re-

search before buying an insurance product because there is no

way known some/other insurers would have charged you any-

thing. eg.

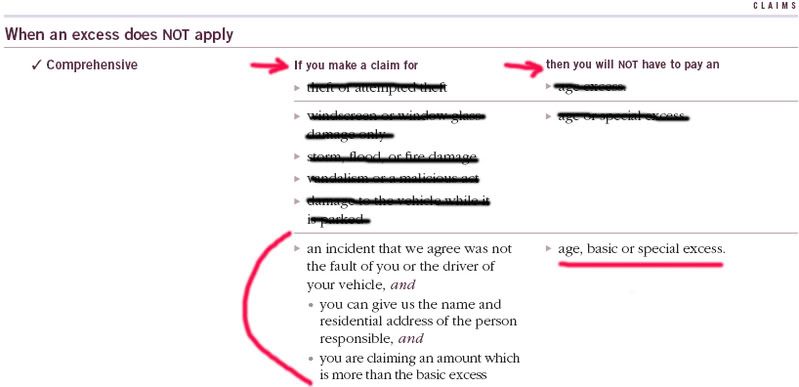

'When an Excess does NOT apply'

Insurer above clearly would not have charged you any excesses

forthe incident you had.

Your Basic Excess is $500, so as long as the damage is more

than your excess & you were not at fault, a Nil excess is

applicable.

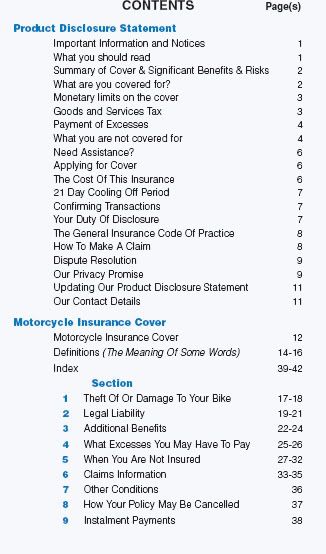

Now if you have a look at your PDS, you will find the following.

1. An Excess is payable

2. Inexperieced Excess is payable (if its noted on your Certificate)

3. 'When an Excess does NOT apply' does not exist with QBE

No where will you find where a Standard Excess is not payable

or waived as others insurer do.

See Index of PDS below

You make a claim with QBE they'll ask you to pay all applicable

excesses & they correctly advised, its not likely you'll get it back.

They told you about it when you bought the product. You had a

3 week cooling off period if you didnt. Once that time expired you

agreed to the T&C bud

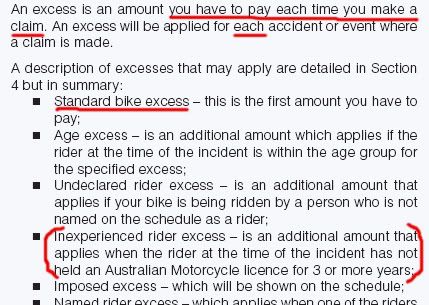

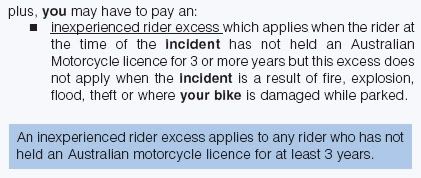

See below:

The only time an Inexperienced rider excess would

not apply is as below:

Bit of trivia: QBE are big on excesses!

The word is mentioned no less than 60 times in their PDS

1. I'm not renewing with wQBE as they won't waive my excess, 2. I would not recommend them to anybody... 3. certainly not unless you fully read and understand their PDS. 4. I'm going to find a decent third party insurer and save my wasted $$$$

MG wrote: 1. That was never going to happen bud

2. No worries

3. 100% correct. You may not have gone with em to begin

with if you did just that

4. Makes sense

If I could just add a coupla last pointers (not directed to you)

about excesses/insurers etc

Excesses have one use only, & that is to remove the ability of

the customer to make small claims - small as in dollar value.

If we didnt have excesses & could make small $XXX.00 claims,

the cost of insurance across the board would skyrocket.

Unfortunately given your incident, damage, your insurer & their

guidelines, lodging a claim without it not costing you anything

was always going to be out of the question

Some insurers will offer a nil basic excess for those 50 & over

because this age group are statistically less likely to lodge claims

and these are only for selected lines of insurance eg home/car.

I'm not aware of any insurers who offer a nil excess for motor

cycles even for over 50yo's.

Some of those that do offer nil excess for clients under 50 do so

at a cost eg $270 more than if you chose to have a Basic excess.

I've said it so many times already but I'll say it again. COST of

insurance is not or should not be the most important factor. It is

important but it shouldnt be the sole factor in deciding who

to insure with.

In this thread I illustrate how InsureMyRide offer a Policy HALF the

price of what I'd been paying.

If cost was the most important factor I'd have bought a Policy

off em then & there but I didnt. Why?

X wrote:They've got 25% off if you book online at the mo, only prob is they only do market value + $2k for mods. If it wasn't for that I have gone with them and saved myself another $500pa!!Cost of a Policy is going to be irrelevant if you have the worst caseMG wrote:That & more..

I checked my notes, had another look thru their booklet, read previous posts

on here about em, read my emails from em & theres still more I need to clarify

with em.

IMHO I think they have an inferior product compared to whats available out there.

There are a number of things I don't like eg.

Replacement bike - First 12mths of reg only, whereas these day 2yrs

is standard, so if I insure with them, no replacement at all.

Pro's are they are part of Suncorp so have strong backing & they are charging

$1000 less which is huge!

But cost is not the most important thing to me. I'd rather pay a couple

hundred more to get the cover I want. I'll still have to do some more

work & weigh it all up before deciding.

senario & you are not placed back in the same position you were in

before the incident took place.

Thats what it comes down to & thats what insurance is all about. Some

can do it better than others.

I believe that these policies and practices are fairly standard across the motorcycle insurance board (perhaps MG could provide some light).

MG wrote:I dont hold the same views champ.

That practice is certainly not standard across the board, as

shown above.

Putting premiums aside, I've yet to come across an insurer or PDS

which was 2nd to none. I challenge anyone to prove otherwise.

Because any PDS available will have something that is at worst,

inferior or less to what another insurer gives or at best, is given

by others.

The fact is, All insurers have their pro's & con's. It is for us to

determine what they are & weigh all factors before making a decision.

At days end, I know it sucks (your situation) & I feel for ya but unfort-

unately it doesnt take one long to realise your gripe against QBE is

unfounded. They have not acted against the T&C that you agreed to.

-

robracer

- VIP MEMBER

- Posts: 15251

- Joined: Thu Feb 24, 2005 8:23 pm

- Bike: ZX6R

- State: New South Wales

- Location: Port Macquarie

Re: Latest Insurance Quote

Shit ....thats right I seem to recal that You work in or had worked in this industry MG

Re: Latest Insurance Quote

Hi Mikemike-s wrote:Agreed, i got the gsx250 registered today and when i got 3pp insurance i was asked the whole raft of questions about my driving history, suspended/disqualified.

I figured to hell with it and admitted that i got suspended for 3 months for speeding.

Surprisingly i don't believe that it made an impact on how much it cost me for the insurance. I did an estimate earlier and it came across as $19/month when i did an online estimate. In reality it cost me 20.54 a month. Which is pretty close (just on 10% more). I would have expected maybe 25/month, but i guess its not made as much of an impact as i thought.

All depending on the insurer & how they calculate premiums. My experience tells

me driving infringements usually have a more pronounce effect on excesses.

ie imposed special excesses rather than premiums.

Insurers do not check your driving history, however come claim time, if there is any

indicators which would lead them to check, you will be asked to sign a consent form

for them to obtain details from VicRoads or applicable Gov body for other states.

Failure to provide consent is sufficient for your claim to be reduced, denied or in worst

cases, your policy cancelled as tho it never existed. Provide consent & they'll soon find

the truth. Either way it will affect you.

Once spoke to a young fella who wrote off his $60k sports car. His claim was denied

because he had one more driving infringement than what he'd disclosed.

Can be costly not disclosing whats required.

-

Seth

- Newbie

- Posts: 20

- Joined: Fri Nov 13, 2009 12:02 pm

- Bike: Ninja 250

- State: Please Select a State

Re: Latest Insurance Quote

Learner's looking to insure my brand new bike. Looking at Insure my Ride but I see that they have 3rd party and theft separate, so if I wanted both do I add the premiums together? Can you get both?

Any other recs for insurance? I've always had cars but as a main driver never as the policy holder, do I still get some sort of rating?

Any other recs for insurance? I've always had cars but as a main driver never as the policy holder, do I still get some sort of rating?